Employee Ownership Tax Credit to Establish or to Expand

The information contained on this page is applicable for new employee ownership conversions (companies without employee ownership plans prior to application date) occurring on after August 7, 2023 (per CRS 39-22-542).

Pursuant to C.R.S. § 39-22-542(6), OEDIT has the sole authority to determine eligibility through any stage of the EOTC program process, including but not limited to reviewing applications, assessing completeness, verifying business and employee-owned business qualifications, determining cost eligibility, and reserving and issuing tax credit certificates.

Program Summary

The Employee Ownership Tax Credit to Establish or to Expand is available to current Colorado-headquartered businesses and their employees to provide an incentive to establish or expand eligible employee ownership structures: employee stock ownership plan, worker-owned cooperative, employee ownership trust, LLC membership, phantom stock, profit interest, restricted stock, stock appreciation rights, stock options, or synthetic equity. The tax credit covers up to 50% of a qualified business’ conversion costs for use on their state income taxes. To participate in the program, the applying business must be existing in Colorado for at least one year prior to starting their employee-ownership conversion and applying for the tax credit.

In June, 2021, Governor Polis signed into law HB25-1021 Tax Incentives for Employee-Owned Businesses. The bill provides $10 million annually in tax credits to fund professional service costs of conversion to employee ownership. The program makes employee ownership conversions more accessible for businesses throughout Colorado. The program and funding are available for the next 5 years, closing on December 31, 2026.

In May, 2023, Governor Polis signed into law HB 23-1081, which expanded the program eligibility criteria. The expansion bill provides four of the following updates to the program (more details can be found in the lower sections of this program page, under the “Eligibility” accordion):

- Increases the cap for converting a qualified business to a worker-owned cooperative or employee ownership trust from $25,000 to $40,000, and increases the cap for converting a qualified business to an employee stock ownership plan from $100,000 to $150,000;

- Effective for applications dated on or after January 1, 2024: Expands the tax credit to include 50% of the costs of a qualified employee-owned business expanding its employee ownership by at least 20%, not to exceed $25,000;

- Expands the tax credit to include 50% of the costs of a qualified business converting to or expanding an alternate equity structure, not to exceed $25,000. An alternate equity structure is a mechanism under which an employer grants to employees a form of employee ownership, including LLC membership, phantom stock, profit interest, restricted stock, stock appreciation right, stock option, or synthetic equity. The bill establishes certain minimum requirements for an alternate equity structure and requires the Colorado office of economic development in the office of the governor to develop guidelines for the types of employee ownership grants that qualify as an alternate equity structure.

- Specifies that a qualified business or qualified employee-owned business may apply for and claim only one credit for the conversion or expansion costs per tax year.

To access our service provider directory or find resources to support your business’ conversion for this program, or any of our employee ownership programs, please contact us.

This program is now open for applications. Please view the "eligibility" and "how to apply" sections below to get started.

Overview

Type: Tax credit

For: Colorado businesses converting to employee ownership

Amount: Up to $25,000, $40,000, or $150,000

Application period: Open and accepted on a rolling basis

OEDIT division: Colorado Employee Ownership Office

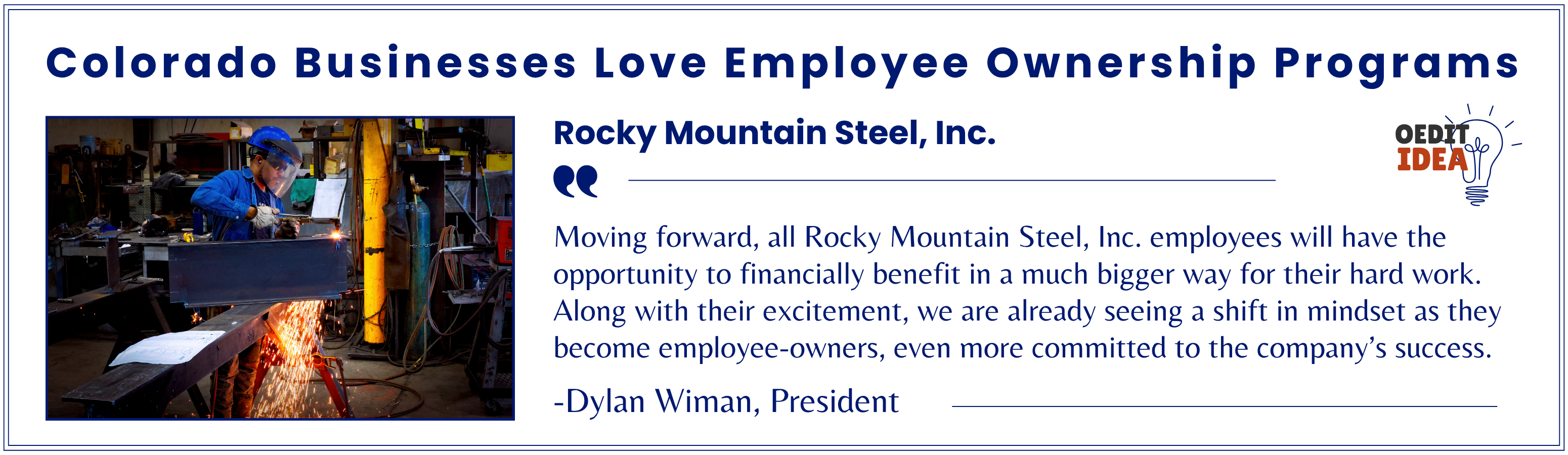

Image description: Business testimonial highlighting that Colorado businesses love employee ownership programs. Quote from Rocky Mountain Steel, Inc. President, Dylan Wiman, “Moving forward, all Rocky Mountain Steel, Inc. employees will have the opportunity to financially benefit in a much bigger way for their hard work. Along with their excitement, we are already seeing a shift in mindset as they become employee-owners, even more committed to the company’s success.”

Current Colorado-headquartered businesses converting to employee ownership between January 1, 2022 and December 31, 2033 may be eligible to apply. Eligible structures include: employee stock ownership plan, worker-owned cooperative, employee ownership trust, LLC membership, phantom stock, profit interest, restricted stock, stock appreciation rights, stock options, or synthetic equity. Businesses must apply for this tax credit prior to completing their employee ownership conversion. Typically, the conversion to an employee-owned structure takes between 6-12 months to complete.

To be eligible for this program, qualified businesses must:

- Be converting to an entity type offering at least 20% equity in the business to employees (excluding founders)

- Have at least 3 full-time employees (or 3 members, if a cooperative)

- Be headquartered in Colorado for at least 1 year

- Be in operation for at least 1 year

- Be in good standing with the Secretary of State

- Not have applied for this program more than once in a calendar year

- Once a tax credit has been reserved, the business has 18 months to demonstrate that at least 20% of the total costs have been incurred

Eligibility for a staged conversion

A staged conversion means that the initial application will include a minimum of 20% equity in the business being offered to employees. If you do not use the entire tax credit with your initial application and decide to add a minimum of an additional 20% of equity in the future (while the program remains open and funds are available), you may be eligible to access any remaining tax credits.

Businesses considering a staged conversation in the future must indicate it in their application. If a staged conversation is approved, you must share at least an additional 20% equity with employees with each additional stage to access any remaining reserved tax credits.

HB 21-1311, which established the tax credit, defines each structure the following way for the purposes of this program:

- Employee stock ownership plan: as defined in section 4975 (e)(7) of the internal revenue code, as amended

- Worker-owned cooperative: as defined in section 1042 (c)(2) of the internal revenue code, as amended

- Employee ownership trust: an indirect form of employee ownership in which a trust holds a controlling stake in a qualified business and benefits all employees on an equal basis

HB23-1081, which broadened the tax credit, defines additional eligible structures in the following manner for the purposes of this program:

- Alternate equity structure" means a mechanism under which an employer grants to employees a form of employee ownership, including but not limited to an employee stock purchase plan, LLC membership, phantom stock, profit interest, restricted stock, stock appreciation right, stock option, or synthetic equity.

- An alternate equity structure must at a minimum:

- Grant rights to or be offered to at least twenty percent of an employer's eligible workers, or grant rights to or be offered to at least twenty percent of eligible workers of an employer that is owned by or operated for the benefit of eligible workers in a broad-based employee ownership transition.

- "eligible workers" means all full-time employees, regular employees, non-seasonal employees, non-managerial employees, and contract labor.

- Have the participation of at least twenty percent of an employer's eligible workers.

- Allocate at least twenty percent of the fully diluted securities or rights to a synthetic interest in securities to participating eligible workers, or allocate twenty percent of net profit from operations to participating eligible workers.

- Grant to participating eligible workers informational rights, decision-making rights, and non-financial rights that are equal to or greater than the rights that are granted to holders of the employer's common stock or holders of the employer's residual membership interest.

- Grant rights to or be offered to at least twenty percent of an employer's eligible workers, or grant rights to or be offered to at least twenty percent of eligible workers of an employer that is owned by or operated for the benefit of eligible workers in a broad-based employee ownership transition.

Eligible expenses include:

- Accounting services

- Business valuation services

- Legal services

- Succession planning services

- Technical assistance

Eligible expenses must be approved by a Certified Public Accountant that is not affiliated with the owner of the qualified business.

The tax credit amount will be calculated based on expenses of professional services required to transition the business to one of the recognized employee ownership structures. See the above section for included expenses.

For newly established employee ownership structures, businesses may be issued tax credits of up to 50% of their conversion costs, not to exceed:

- $25,000 for Alternative Equity Structures (i.e., LLC membership, phantom stock, profit interest, restricted stock, stock appreciation rights, stock options, or synthetic equity),

- $40,000 for Worker-Owned Cooperatives and Employee Ownership Trusts,

- $150,000 for Employee Stock Ownership Plans.

Effective for applications dated on or after January 1, 2024: For businesses increasing the % of their their employee ownership plans (by a minimum of 20%), businesses may be issued tax credits of up to 50% of their conversion costs, not to exceed:

- $25,000 for employee stock ownership plan, worker-owned cooperative, employee ownership trust, LLC membership, phantom stock, profit interest, restricted stock, stock appreciation rights, stock options, or synthetic equity.

If your certified expenses are more than the amount of tax credits reserved, we will issue an overage for the difference. This is subject to annual limits up to the maximum allowable tax credit by structure type. If your certified expenses are fewer than the tax credits you reserved during pre-application, we will calculate your tax credit based on your actual expenses.

The tax credit certificates must be used in full during the tax year in which the conversion to a qualified equity structure is completed. Any unused credits will be refunded.

This program is now open for applications and will be reviewed in order of receipt.

You must complete the pre-application and application for reservation prior to completing your employee ownership conversion to qualify for the tax credit, otherwise your application will become ineligible. We encourage you to apply before starting the conversion or during the early stages of the conversion. Please note that converting to an employee-owned structure typically takes between 6-12 months to complete.

Step 1: Complete and pass the pre-application

Log in or create a new account in the OEDIT application portal. To protect your personal information, we manually add users to the portal, so please allot up to several days for us to activate your account.

If your answers to the pre-application qualify your business, you will receive an email confirmation of approval. Follow the steps outlined in the email to access the next step.

To meet initial eligibility requirements as a qualified business, you must disclose which structure type you are converting to (employee stock ownership plan, employee ownership trust, worker-owned cooperative, or alternate equity structure).

Step 2: Apply for reservation of tax credit

After your eligibility is confirmed, the system will automatically create a reservation application for you to complete. To access your application:

- Go to the application portal

- Once logged in, click the "Employee Ownership" tile.

- On the following page, click the “Employee Ownership Tax Credit Pre-Qualification” tile.

- Complete all required fields on each page and click “Next” on the lower right of the page to progress through the application.

- At any time, you may save your progress and continue the application process later by clicking the “Save for Later” link on the lower left of each application page.

- A determination of eligibility will be made once the pre-qualification application has been submitted.

- Once approved, please note the PAR file number within the “Success Message” from the prior step, to open the Reservation Application that was generated from the Pre-qualification approval.

- Please complete all required fields on each page of the application, uploading any required files and clicking “Submit” once completed.

- Within 90 days, the Office will review your application and make a determination regarding the reservation of tax credits for your conversion.

For this step in the application process, you will need to provide:

- Certificate of Good Standing from the Secretary of State showing your existing business structure (or proposed newly forming worker-owned cooperative)

- C corporation

- S corporation

- Limited Liability Company

- Partnership

- Limited Liability Partnership

- Sole Proprietorship

- Or other pass-through entity

- Information on whether you will be applying for a staged conversion in addition to initial conversion

- Federal Employer Identification Number, Colorado Account Number, or Individual Taxpayer Identification Number

Step 3: Apply for tax credit issuance

When your conversion is complete, and you are prepared to file an issuance report to claim the tax credits:

- Navigate to the application portal.

- Once logged in, select the “Employee Ownership Tax Credit” tile. On the following page, please click on the “Applications” tab on the top left of the screen and again select “Applications” from the resulting drop-down menu.

- On the following page, click on the “AI” file listed under the “Funding Awards” header on the lower right side of the screen. When this file opens, scroll down to the bottom of the page and under the “Issuance Report” heading click on the “Next” button on the lower right to begin entering the information for all tax credit recipients for the issuance request application.

- Click “Add” to the right of the “Pass-Through Entities” heading to provide information for each additional tax credit recipient. You will need to repeat this until all passthrough entities have been entered. When all information has been entered, click “Next” at the bottom right of the page to continue completing the remainder of the report.

- Once the Issuance Report has been submitted you will be contacted within 90 days, and if approved, the tax credits will be delivered to each recipient via email.

- Once received, please download the tax credit certificate and save it to a secure place where you will remember where to find it.

You will need to provide the following 4 documents for issuance of the tax credit:

1. A letter (as a PDF) signed by a 3rd party CPA that attests:

- The expenses listed on the Expenditures Worksheet, (xlsx): (included in the letter) were in conjunction with the employee ownership conversion.

- The dates of the expenses are accurate and occurred in your conversion time period.

- You will need to supply the canceled checks to the CPA that match the list of expenses in the Expenditures Worksheet.

- The total amount spent on the conversion is accurate.

- The costs were incurred by the applying business

- Citation to CRS 39-22-542 that the company's expenses are qualified and eligible.

- Here is a sample letter for your reference: Sample CPA Letter, (Google Doc)

2. Please fill out the Form Legal Opinion Sample Letter, (Google Doc) and save as a PDF; this form must be signed by an attorney. Additionally, fill out the Officers Certificate Sample Letter, (Google Doc) and save as a PDF; this form will need to be signed by an applying company executive.

3. Initiating-owner(s) tax identification and contact information document (as a PDF or Word document)

4. Proof of employee ownership conversion documents (as PDFs):

- These may include:

- Notarized Corporate Resolution: establishing the new employee ownership structure type

- Notarized Stock Purchase Agreements

- Articles of Incorporation

- For ESOP - Initial Census Report of participants of the trust (showing employee names of those participating in the ESOP)

- For ESOP - Capitalization Table from before and after the employee ownership transaction

- For ESOP - Summary Plan Description

Step 4: Claim your tax credit

The final step is to claim your tax credit on Colorado state income tax. You will be provided a certificate to be submitted with your Colorado tax return. Colorado allows a variety of refundable and nonrefundable income tax credits. Most, but not all credits are claimed on the Individual Credit Schedule (DR 0104CR).

A tax credit must be used for the tax year that the conversion to a qualified, employee-owned structure (i.e., ESOP, Co-op, EOT, or other alternative equity structure) was officially completed. This date will be verified by the legal documents provided by the applicant as well as the third-party CPA attestation. A signed letter from an attorney may be required. The tax credit is not extendable and is only valid for use during the tax year that the qualified conversion is completed. If the tax credit exceeds the tax liability, the remainder will be refunded to the owners. Any credit that is unused during the tax year that the qualified conversion is completed will expire.

We will provide informational sessions for service providers, such as certified public accountants, to be aware of this tax credit and learn how they can support businesses in applying. As we finalize informational session dates and details, we will offer registration here.

Program Manager